Trading volume and value climbed once again but remained below 2023 figures. As auction prices for many Islay whiskies increased, Lagavulin and Caol Ila experienced significant value gains. Here is the Whiskystats Price Update for September 2024.

Almost 24 thousand bottles of whisky were exchanged at Whiskystats tracked auctions in September 2024. The total trading value (the sum of buyer prices) amounted to €8.6 million, similar to what was observed in July but over €3 million more than in August. On a year-to-year comparison, trading volume was down by 6%, while trading value trailed by 13% from September 2023 figures.

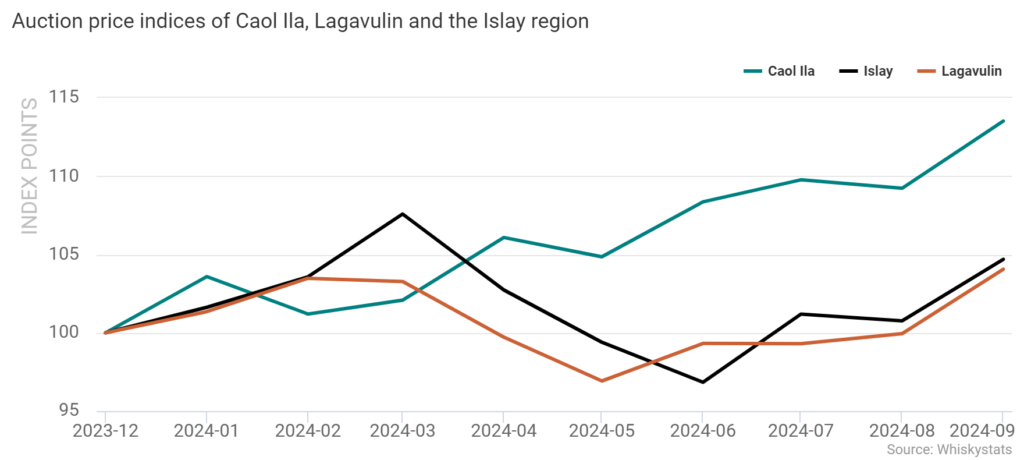

However, the historically 500 most traded whiskies, represented by the Whiskystats Whisky Index, gained 1.5% in value. The best-performing market segment in the September auctions was the Islay region. The Whiskystats Islay auction price index climbed by 3.9% to 234 index points, 9% above its November 2023 preliminary low but still 28% below its April 2022 peak.

Islay Highlights

Lagavulin was among the highest-gaining brands at auctions in September. The 100 historically most traded Lagavulin releases gained 4.1%. At 148 index points, the Lagavulin auction price index returned to the same level seen in February and March of this year. The Lagavulin index previously reached this level in early 2021 before peaking at almost 200 points in early 2022 and then retreating during the market correction phase.

Another well-performing Islay brand was Caol Ila. The 100 whiskies included in the September index movement gained almost 4%. In 2024, the Caol Ila index is currently up by 13.5% in total, making it one of the best performing brands in the overall secondary whisky market. The Caol Ila 1968 Private Collection release from Gordon & MacPhail contributed significantly to the September gain. The auction buyer price jumped back to €6,740 after dropping to €3,600 earlier this year.

Releases such as the above-displayed Lagavulin 1991 Special Release 2012 were responsible for Lagavulin’s September index gain. At the 2022 market peak, some bottles sold for nearly €2,000. In early 2024, however, buyer prices for this Diageo special release dropped below €1,000. But in August and September, it was able to fetch €1.300 and almost €1.500 once again. Also performing well in September was Laphroaig, for which the respective 100 index bottles gained 2.8%.

Islay Lowlights

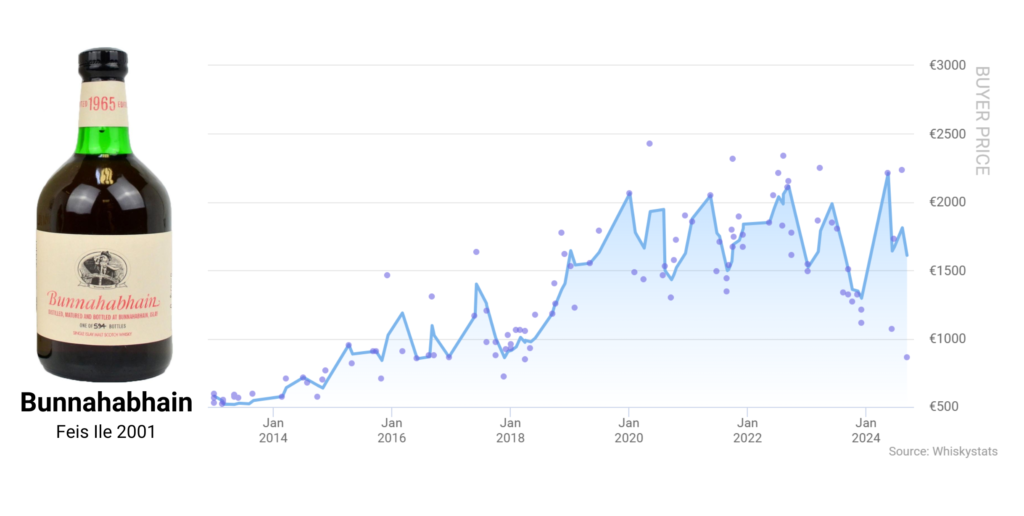

Not all Islay brands performed equally well in September. Octomore (+1.9%), Port Ellen (+1%) and Kilchoman (+1%) trailed behind Lagavulin (+4.1%), Caol Ila (+3.9%) and Laphroaig (+2.8%). Bowmore (-0.3%) and Ardbeg (-0.7%) lost slightly. However, the most severe losses were observed for Bruichladdich (-2.1%), Port Charlotte (-3.1%) and Bunnahabhain (-3.4%).

As the auction price indices suggest, these three brands have not gained strong secondary market traction. For Bunnahabhain, auction prices increased slightly back in 2018 but then stayed rather flat during the whisky market peak before following the overall downward trend. This pattern is exemplified by the above-displayed Bunnahabhain Feis Ile 2001 release. Auction prices consistently hovered around €2,000 over the past four years but have now dropped at times to €1,000.

Activity in the secondary whisky market is clearly increasing again. Become a Whiskystats member to stay on top of the market.

Disclaimer: The whisky market insights presented in this article are based on the Whiskystats database at the time of publication. Whiskystats is constantly adding new data; therefore, some charts and figures may not match after initial publication.